Debiasing Audit Judgment with Accountability

Published in : 1993

Researcher : Jane Kennedy

Research Variable : Audit Judgment, Accountability

Methods

Two subject groups were used. One consisted of 58 executive M.B.A. students at Duke University, all of whom had completed the M.B.A. core course in financial accounting and therefore should be familiar with the accounting concepts used in the experimental materials. Subjects had, on average, 5.5 years of business-related experience. The other group consisted of 171 auditors attending managers' training sessions for a Big Six firm. On average, subjects had been directly involved in six audits in which, as part of an audit team, they judged a client's ability to continue as a going concern. Subjects in both groups were randomly assigned to treatment conditions. Experience did not differ across conditions for either subject group.

The experiment was conducted in a group setting. After subjects read the general instructions, evidence was presented via an overhead projector to ensure that all subjects read the items in the order in- tended, had the same exposure time, and had no opportunity to look back and reread the evidence in some other order. Each slide showed one piece of evidence for nine seconds.9

The task required subjects to judge the likelihood that a firm would fail (i.e., enter bankruptcy proceedings) within one year based on eight pieces of evidence-four supporting failure and four supporting via- bility.10 The items are listed below, where F (V) indicates that the item supports failure (viability).

1. The firm's major product is generally considered to be of good quality. (V)

2. Management states that it is possible that a key patent may be obtained in the near future. (V)

3. This year the company reported a positive cash flow from operations. (V)

4. In general, suppliers of the firm indicate that usual trade credit to the firm will be available. (V)

5. This year the firm reported a significant loss from operations. (F)

6. It appears that if needed it will be difficult to obtain additional debt capital. (F)

7. Discussions with management indicate that a material liability from litigation is likely this year. (F)

8. Management believes there is a good chance of losing a major customer. (F)

To provide a common base rate of failure, subjects were told before considering any firm-specific evidence that the likelihood the firm would fail was 50%. After subjects read the firm-specific evidence, they were asked, "How likely do you think it is that this firm will fail (i.e., enter bankruptcy proceedings) within one year?" Subjects responded on a 0-100 scale, with endpoints labeled "certain this firm will not fail" (0) and "certain this firm will fail" (100) and the midpoint labeled "completely uncertain." The likelihood judgment is the dependent variable. Subjects also completed a brief post experimental questionnaire which included a number of questions designed to check the accountability manipulations.

A 2 x 3 x 2 (order of evidence x accountability x complexity) between subjects experimental design was used. The two orders of evidence were (1) evidence supporting viability followed by evidence supporting failure (++++----), and (2) evidence supporting failure followed by evidence supporting viability (---- + + + +).

The three accountability conditions were no accountability, pre-accountability, and post accountability. In the no-accountability conditions subjects were told:

This study concerns how students with your level of education and experience make judgments. Your judgments will be totally confidential and not traceable to you person- ally. Your responses to the materials will be aggregated and averaged with the responses of others to determine general characteristics of judgment. Please do not identify your- self in any way on these materials. Thank you for your cooperation.

The distinction between pre- and post-accountability is the timing of the accountability manipulation. Pre-accountable subjects were told the following, before evidence for the failure/viability judgment was presented:

This study, sponsored by the Fuqua School, is part of an important effort of the School to enhance the effectiveness and efficiency of business practice. We are interested in learning how students at your level of education and experience make judgments, and in assessing the quality of those judgments. Your responses to the following materials will be reviewed and may be selected for a follow-up conference with you and members of the EEMBA Faculty. If you are selected for this conference, you will be asked to explain and justify your responses. Please print your name and phone number in the space pro- vided so that we can contact you. Thank you for your cooperation.

Post-accountable subjects were presented with the same paragraph after evidence for failure/viability, but before the likelihood judgment was required. Two subject groups were used to operationalize task complexity. Auditors evaluate the ability of a client to continue as a going concern on every audit engagement while executive M.B.A. students, on average, have little experience judging the ability of a firm to survive. Although more complex, this task is not unreasonable for executive M.B.A. students given their business interests and educations.

Analysis and Results

Recall that likelihood judgments were elicited on a 0-100 point scale; thus, subjects' judgments may be thought of as percentages. Descriptive statistics for the likelihood

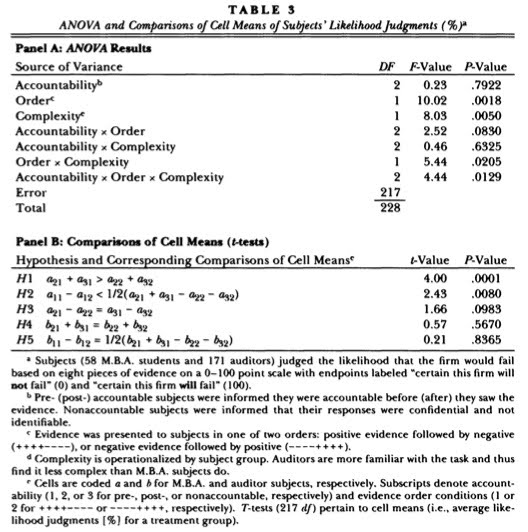

judgments of M.B.A. and auditor subjects are presented in table 2, panels A and B. The analysis-of-variance (ANOVA) and results of comparisons (protected t-tests) of specific treatment (cell) means are in table 3, panels A and B.18

The ANOVA reveals a significant accountability x order x complexity interaction (F = 4.44, p < .01; table 3, panel A). The test for recency among executive M.B.A. subjects shows that post- and non-accountable subjects who receive evidence in a positive/negative order judge the likelihood of failure to be greater than subjects who receive the same evidence in a negative/positive order (means of 60.6 and 72.5 vs. 46.0 and 37.3, table 2, panel A; t = 4.00, p < .0001, table 3, panel B).

Pre-accountable subjects' likelihood judgments exhibit no recency (mean of 48.5 vs. 50.0, table 2, panel A) in contrast to their post-accountable and non-accountable counterparts (t = 2.43, p < .008, one- tailed, table 3, panel B). Accountability clearly moderates recency among executive M.B.A. students. Hypothesis 3 is weakly supported; recency shown by non-accountable subjects is marginally stronger than that shown by post-accountable subjects (difference between means of 72.5 and 37.2 vs. 60.6 and 46.0, table 2, panel A; t = 1.66, p = .10, table 3, panel B).

An analysis of the frequency of subjects adjusting away from the anchor provides results consistent with those above; 93% of post-accountable subjects and 96% of non-accountable subjects adjusted their likelihood of failure judgments away from the anchor while only 68% of pre-accountable subjects did (X2= 15.24, p < .000).19 Moreover, more (fewer) M.B.A. subjects in the positive/negative condition adjusted their likelihoods up (down) than in the negative/positive condition. The proportions of subjects adjusting up (down) are 72% (14%) and 28% (55%) for the positive/negative and negative/positive order conditions, respectively (x2 = 13.14, p < .001).

In contrast to the results obtained from M.B.A. subjects, auditors' judgments show no recency. The difference between the judgments of post- and non-accountable subjects receiving negative evidence last and those receiving positive evidence last is not significant (means of 45.8 and 44.2 vs. 41.4 and 46.3, table 2, panel B; t = .57, p = .57, table 3, panel B). This result is consistent with EoS processing, i.e., the evidence is considered as a set and the anchor is updated once, for the set, rather than for each piece of evidence in the set. Consistent with H5, auditor judgments were not influenced by pre-accountability requirements (mean of 45.6 vs. 43.5, table 2, panel B; t = .21, p = .84). The frequencies of subjects revising up, down, and not revising from the anchor are approximately equal across all conditions, providing further support for no order or accountability effects among auditors.

Future Research

Future research could examine the interaction of accountability with other pressures on auditors such as those mentioned above. The particular accountability "culture" may also be important. For example, accounting firms may have an atmosphere of accountability that affects all facets of an auditor's work.

Alternatively, accountability requirements may be overtly stressed on each task undertaken. Finally, the framework presented suggests potentially effective means of mitigating data-related biases, which may be the more important of the two types of bias because of their immunity to incentive mechanisms.

Summary

Although recency is not expected for auditor subjects who are familiar with a particular task, recency is a well-documented phenomenon in the audit judgment literature. A review of that research indicates that, for the most part, recency is found when subjects were explicitly required to process the evidence in a step-by-step (SbS) mode or when the task was made more complex so that subjects chose a SbS strategy. These studies did not control for accountability requirements, which are common to many audit judgment settings.

This study had subjects make only one judgment after all evidence was presented (EoS), rather than making a judgment after each piece of evidence was presented (SbS). Recency is hypothesized for judges who use a SbS processing strategy to ease the cognitive demands of complex belief revision tasks in an EoS response mode. Executive M.B.A. subjects, unfamiliar with judging the ability of a firm to survive, exhibited significant recency effects while auditors, who are familiar with this task, did not. However, when accountability was imposed on the M.B.A. subjects, no recency effects were noted. Consistent with the framework proposed in section 2, this experiment shows that effort- related biases such as recency can be mitigated by accountability.

There are at least three limitations of this study. First, auditors work in much richer information environments than depicted in the experiment. It is not obvious, however, what impact additional information has on auditors' judgment biases. Second, accountable subjects faced no penalty for providing unjustifiable responses in this experiment, while in an audit environment unjustifiable judgments could result in additional hours worked, reputation costs, etc. Finally, I examine accountability in isolation from other pressures auditors face (deadlines, incentives, and feedback), all of which may interact with accountability (Ashton [1990] and McDaniel [1990]).

This study has implications for auditing practice and audit judgment research because auditors operate in an accountability-inducing environment. Audit managers make going-concern evaluations of clients based on many pieces of evidence that have been gathered and re- viewed, and their own judgments are subject to review. The absence of recency found here, when judgments were made by experienced professionals after all the evidence was available, and the debiasing effect of accountability for less experienced judges suggest that recency may not be an issue of great concern for audit practitioners. Moreover, ex- periments that do not control for accountability may overstate the significance of judgment biases attributable to effort.

haaa.. akhirnya slese ya :D senanknya... tinggal diringkas jadi table.. n dkumpul k Pak Galumbang... masih nyusul satu lg tugas individu dr pak Butar2... smangad amell hahaha..