dah lama abis ga gw sentuh ni blog hahaha...

dah ampir 2 taonan kali ya apa staonan gt...

kabar gue baikkk dan totally awesome meski ditahun 2011 ini banyak bgt masalah2 dan hujan badai but fortunately smuanya da mule membaik di akhir september... :)

thx God 4 everything n sorry bgt Babe klo gw banyak bangeedd nyusahin Babe n bkin Babe sakit ati liat tingkah laku gue yg inappropriate..

untuk masalah percintaan,, gw sdang bersama seseorg saat ini, blm lama sih, sbulanan lebih... n i hope this would be my last kalo yg diatas mengijinkan... :) i'll try my best deh... kalo awal2 pasti masi anged lah ya n blm ad masalah yg trlalu gmana bgt...

let it flow aja d hahah..

gw da lulus kul,, status : pengacara, pengangguran banyak acara :D rencana februari mo ambil kuliah Ak lg di untar, tp kalo jadwalnya dapet malem, nyokap gue ga ngasih, mala suru blajar bahasa k cina aja kt nyokap gw --" entahlah masih bngung hahha..

Minggu, 04 Desember 2011

Senin, 05 Juli 2010

happy birthday daddy :)

ew.. da lama ga nulis2 blog...

jadi kangen corat coret lagiii buat ngucapinn happy birthdayy for my beloved daddy...

you are my everything dad... :)

moga papi panjang umur... selalu sehaaat... rajin berdoaa... sayang sama aku.. mami (n promise that only two of us will stay in your heart)... ga kena pnyakit2 kayak kolestrol, asal urat, diabetes, darah tinggi dsb dsb yang sering diderita orang2 yg umurnya udah stengah abaadd :p tp dah stengah abad juga bokap gw masih narsis ga kalah kyk gue...

gw jadi tau drmana narsis gw ini dturunkan bwakakka...

alhasill karena bertepatan jatohnya dihari minggu.. jadilah kita pergi makan2...

dan si bibeh yang baru aja pulank dari purwekorto dan sampe jakarta jam 8 pagi ini bela2in datenk buat ngucapin happy birthday ke calon mertua nya nan narsis itu hahaha...

malemnyaa kita makan barenk lagii ditemani sekuntum mawar merah dan sebuah lilin dwonk wew da kayak candlelight dinner ber4 aje bwahahah tp seruu... bwahahha lupa bawa kamera tapi 0.o

uhmm my only wish for his birthday iss.. god always take care of him, watch for his life journey, give him prosperity, health and happiness... and pleaasee God, don`t take my daddy away from me and my mommy before he can accompany me when i`m graduate, married and have kids... need you for my life journey dad and with you i always have a new moment, new things to learn, new things to make me mature and understand how to face life...

FAMILY = father and mother i love you <3

Suri Cruise, putri Tom Cruise berusia 3 tahun yang dah modis abess!! haha

gue salut banget ma ni anak.. umurnya baru 3 taon ajaaa dah modis abess...

umur 3 taon da blanja lip gloss... baju n dress nya dirancank ama designer ternama...

susah la ya namanya anak artisss hahaha...

ni penampakkannya...

hwahahahah mantaab gaan gw aja umur 3 taon masi maen masak2an.. dokter2an dan mlakukan hal2 autis laennya hahahah...

uda sampe masa2 puber aja die...

umur 3 taon da blanja lip gloss... baju n dress nya dirancank ama designer ternama...

susah la ya namanya anak artisss hahaha...

ni penampakkannya...

hwahahahah mantaab gaan gw aja umur 3 taon masi maen masak2an.. dokter2an dan mlakukan hal2 autis laennya hahahah...

uda sampe masa2 puber aja die...

Selasa, 04 Mei 2010

Selamat Jalan teman... T___T

gw cuman mo bilank turut berduka cita sedalam2nya buat tmen gw Ricky Thoriq Pramujati... semoga amal ibadahnya diterima di sisi Yang Maha Esa...

denger2 sih katanya gara2 kecapean.. jadi selama seminggu ini dia sibuk ngeband bikin album.. pulank ampe rumah jam 2.. trus lanjut belajar sampe jam 5... trus baru tidur jam 5 ampe jam 9...

hari sabtu minggu dia kcapean n skarat , masuk rumah sakit... minggu sore da bole pulang padahal... taunya pas makan malam jam 8 dia tiba2 muntah2 n kejang.. pas dibawa ke ugd dah ga ketolong lagi...

anaknya pinter , baik dan dewasa... selama ini dia selalu jadi guru besar kita kalo ada pelajaran atau hal apapun yang kita ga ngerti jalan keluarnya...

hal terakhir yang gw inget itu pas dia minjem catetan audit buat disalin dan dikumpul... saat menjelang ujian dia sering nanya2 bahan dan minjem catetan ke temen ane.... ga akan terulang lagi T___T

kesehatan emang harta paling berharga ya.........

bye thor... pasti lu dah seneng disana!

denger2 sih katanya gara2 kecapean.. jadi selama seminggu ini dia sibuk ngeband bikin album.. pulank ampe rumah jam 2.. trus lanjut belajar sampe jam 5... trus baru tidur jam 5 ampe jam 9...

hari sabtu minggu dia kcapean n skarat , masuk rumah sakit... minggu sore da bole pulang padahal... taunya pas makan malam jam 8 dia tiba2 muntah2 n kejang.. pas dibawa ke ugd dah ga ketolong lagi...

anaknya pinter , baik dan dewasa... selama ini dia selalu jadi guru besar kita kalo ada pelajaran atau hal apapun yang kita ga ngerti jalan keluarnya...

hal terakhir yang gw inget itu pas dia minjem catetan audit buat disalin dan dikumpul... saat menjelang ujian dia sering nanya2 bahan dan minjem catetan ke temen ane.... ga akan terulang lagi T___T

kesehatan emang harta paling berharga ya.........

bye thor... pasti lu dah seneng disana!

Senin, 15 Maret 2010

SafaRi :D

yeyy... Liburan hari minggu kmariin sangat menyenangkan... haha...

k taman safari,, bw makanan yg buaanyak. bw mami papi n bw pacar..smua trasa lengkap dihati.. nyampe safari jam 12,, gw da kebelet boker,, alhasil gw boker d WC taman safari,, gw kira jorok ternyata bersihhh gyahahaha aernya dingin... maknyus dah..

abis boker makan dulu.. ayam bakar cumi bakar sate bakar.. tp smuanya gaenak dan mahal --` cih.. abis ituu gw jalan2 sama bibeh,, ke goa baby zoo.. didalemnya banyak burung2 yg warnanya macem2 trus mreka jinak.. mau dket2 ama orank gyaahahha senankkk.. trus kluar dr goa burung itu ada anak macan, anak singa n anak harimau.. gw ama bibeh poto2 ama tu macann ahahah senank... tu macan dah bunyi grao grao gt .. berat pula ampe sakit paha gue pangkunya.. T.T tiap sebelom poto, bibeh slalu nanya ke mas nya ,"udah dkasih makan siang mas?" bwakakakak~ poto2nya silahkan diliat d pesbuk saya..

udah gituu kita ke haunted mansion hahaha naek kreta gitu berdua2, didalemnya ada pocong kuntilanak tengkorang sundel bolong dan kawan2.. sangat gelap dan mengerikan, didalemnya dngin banget pula --`

gyahahah abis itu nonton safari show bentar,, orangutannya pinter dan,. trus ada anjing pom nya jg~ abis tuu liat pinguin.. lucu2 dah pgn gw cekek satu2 abisnya gemes,, tp masa masukya 100rb per orank cih mahal bwaanget mendink gw liat dari luar aja trus poto2 wkakaka.. abis tuu muter2 bentar n pulank dweh.. tdnya mw langsung tancap ke taman bunga tp kagag kburu dah ksorean,,, hahaha impian gw dari lama dh terwujud juga ya... bisa jalan2 sama pacar dan kluarga gw, kluarga dia.. okelah tq babe Jesus ^^ tinggal nginep bareng aja nihh sekeluarga belum tercapai,,, :) soon..

k taman safari,, bw makanan yg buaanyak. bw mami papi n bw pacar..smua trasa lengkap dihati.. nyampe safari jam 12,, gw da kebelet boker,, alhasil gw boker d WC taman safari,, gw kira jorok ternyata bersihhh gyahahaha aernya dingin... maknyus dah..

abis boker makan dulu.. ayam bakar cumi bakar sate bakar.. tp smuanya gaenak dan mahal --` cih.. abis ituu gw jalan2 sama bibeh,, ke goa baby zoo.. didalemnya banyak burung2 yg warnanya macem2 trus mreka jinak.. mau dket2 ama orank gyaahahha senankkk.. trus kluar dr goa burung itu ada anak macan, anak singa n anak harimau.. gw ama bibeh poto2 ama tu macann ahahah senank... tu macan dah bunyi grao grao gt .. berat pula ampe sakit paha gue pangkunya.. T.T tiap sebelom poto, bibeh slalu nanya ke mas nya ,"udah dkasih makan siang mas?" bwakakakak~ poto2nya silahkan diliat d pesbuk saya..

udah gituu kita ke haunted mansion hahaha naek kreta gitu berdua2, didalemnya ada pocong kuntilanak tengkorang sundel bolong dan kawan2.. sangat gelap dan mengerikan, didalemnya dngin banget pula --`

gyahahah abis itu nonton safari show bentar,, orangutannya pinter dan,. trus ada anjing pom nya jg~ abis tuu liat pinguin.. lucu2 dah pgn gw cekek satu2 abisnya gemes,, tp masa masukya 100rb per orank cih mahal bwaanget mendink gw liat dari luar aja trus poto2 wkakaka.. abis tuu muter2 bentar n pulank dweh.. tdnya mw langsung tancap ke taman bunga tp kagag kburu dah ksorean,,, hahaha impian gw dari lama dh terwujud juga ya... bisa jalan2 sama pacar dan kluarga gw, kluarga dia.. okelah tq babe Jesus ^^ tinggal nginep bareng aja nihh sekeluarga belum tercapai,,, :) soon..

Sabtu, 02 Januari 2010

New year holiday..

aghh..

gw palink snenk natalan n taon baru... karena keduanya muncul di tanggal yg berdekatan n rasanya taon baru jadi makin meriah kalo barengan ama natal, jadi ada pohon natalnya ama ada lampu warna -warni gitu gyahahahah..

slma liburan kmrn dr tgl 30 ampe tgl 1 gw pegi k bandung..

sama kluarga gw, bibeh,, n nyampe sana ketemu sama kluarganya bibeh..

brangkat dari hum tanggal 30 jam 11 an.. si mike ikut gw soale kluarganya datenk dr purwakarta ^^

sampe disana kita nganter mike dulu ke guess house tmpat si mike nginep.. dan pastinya lah dsana mampir sbentar ktmu sm bonyoknya..

dah sore tu jam 4,, ni pertama kali gue ktemu nyokapnya.. kalo ktmu bokapnya dah 2 kali..

gw diajak jalan sama nyokapnya n bakal dianter balek khotel tmpt gue nginep (di mason pine padalarang).. tp gw mrasa kek nya repotin gitu dah sore, trus malem nanti anter gue pulank.. mana padalarang tu mesti masuk tol..

akhirnya g blg gausah tante,. repotin..

trus tantenya bilank,, yaudah besok yaa kamu jalan2 sama kita.

ew.. akhirnya gw cuman bilank.. eh.. um.. yaa..udah d tante hahahahaa~ *takut*

besoknya.. tanggal 31 desember..stelah breakfast jam 10 di hotel (gue makan dimsum, pancake, dll), kita langsung brangkat kbandung, kita ktemuan disana rencananya (di apartment tante gue di majesty dket maranatha).. dan jadilah kita berjalan2 ber5! sama cecenya jugah! hahaha takut..

itu baru ptama kali juga gw ktemu cecenya.. ktemunya dikos.. dkos ce2nya ad anjing lucu bannggeeeeett hweeh kek na anjing shin tzu deh.. kpalanya dikuncir gt sumpah lucu abis.. pas pntu kamar kebuka tuh anjing dah langsung lari2 aja nyamperin smua orank.. kek anak anjing autis hahaha sumpah gue gemes abis..

akhirnya stelah dr kost ce2nya.. kita makan siang di rumah makan mandarin. (namanya emg gtu) dsana gw dcekokin berbagai macam makanan sama emaknya -.- OMg ampe buncit gw, ga pernah gw sekenyang itu, tp mau ga mau mesti diabisin dah..

abis makan kita pergi ke secret fashion.. dsuruh pilih baju tp gagenak gw.. gw tolak2 sebisa mungkiinn HHHHHHHHAAAAAAAAAA!!! gagenak abis sumpah --` akhirnya dipaksa pilih.. no.. akhirnya jadi lah 2 pcs tuh baju.. dkasih sama emaknya .. gw langsung cpet2 sms nyokap gue. "mami beliin oleh2 yuk buat si mike n kluarga, gaenak aku dbeliin baju sgala" gyahaha.. dah tu.. abis tu masih ke mol rencana mo nonton avatar 3d tp penuh tmptnya,, kaga jadi d.. akhirnya kita smua balek k guess house tmpat mke nginep.. dsana duduk2 smbil ngobrol2.. jam 7 pergi makan seafood.. makan cumi, kepiting, kerang ampe 2 piring masing2 yg ada dimeja.. kembali gw dicekokin sama kerang, cumi2 suruh abisin n kepiting 1 ekor + 3 capitnya yg gede itu --`

pulank makan jam 8.30 gue lsg dianter k hotel gue nginep.. disana bner2 melentung perut gue..stelah pamitan dll mreka lsg pulank.. krn waktu tu nyampe hotel gue dah malem juga gt..

meskipun kenyang n perut melentung,tp tetep ajah jam 12 gue makan lagi krn dhotel gue ada acara taon baruan hahaha.. sayanknya tgl 1 gue da harus pulank .. pdahal tgl 1 diajakin nonton sm cecenya juga n sm ko alex(pacar ce2nya) sayank dobel date ga ksampean.. --`

kapan yank kita liburan bareng lage hahaha...

yah gw ngerasa srek kok sm kluarganya.. sangad welcome.. smoga nanti kita bs ktemu lagi ya om, tante, cece.. hahaha XD

gw palink snenk natalan n taon baru... karena keduanya muncul di tanggal yg berdekatan n rasanya taon baru jadi makin meriah kalo barengan ama natal, jadi ada pohon natalnya ama ada lampu warna -warni gitu gyahahahah..

slma liburan kmrn dr tgl 30 ampe tgl 1 gw pegi k bandung..

sama kluarga gw, bibeh,, n nyampe sana ketemu sama kluarganya bibeh..

brangkat dari hum tanggal 30 jam 11 an.. si mike ikut gw soale kluarganya datenk dr purwakarta ^^

sampe disana kita nganter mike dulu ke guess house tmpat si mike nginep.. dan pastinya lah dsana mampir sbentar ktmu sm bonyoknya..

dah sore tu jam 4,, ni pertama kali gue ktemu nyokapnya.. kalo ktmu bokapnya dah 2 kali..

gw diajak jalan sama nyokapnya n bakal dianter balek khotel tmpt gue nginep (di mason pine padalarang).. tp gw mrasa kek nya repotin gitu dah sore, trus malem nanti anter gue pulank.. mana padalarang tu mesti masuk tol..

akhirnya g blg gausah tante,. repotin..

trus tantenya bilank,, yaudah besok yaa kamu jalan2 sama kita.

ew.. akhirnya gw cuman bilank.. eh.. um.. yaa..udah d tante hahahahaa~ *takut*

besoknya.. tanggal 31 desember..stelah breakfast jam 10 di hotel (gue makan dimsum, pancake, dll), kita langsung brangkat kbandung, kita ktemuan disana rencananya (di apartment tante gue di majesty dket maranatha).. dan jadilah kita berjalan2 ber5! sama cecenya jugah! hahaha takut..

itu baru ptama kali juga gw ktemu cecenya.. ktemunya dikos.. dkos ce2nya ad anjing lucu bannggeeeeett hweeh kek na anjing shin tzu deh.. kpalanya dikuncir gt sumpah lucu abis.. pas pntu kamar kebuka tuh anjing dah langsung lari2 aja nyamperin smua orank.. kek anak anjing autis hahaha sumpah gue gemes abis..

akhirnya stelah dr kost ce2nya.. kita makan siang di rumah makan mandarin. (namanya emg gtu) dsana gw dcekokin berbagai macam makanan sama emaknya -.- OMg ampe buncit gw, ga pernah gw sekenyang itu, tp mau ga mau mesti diabisin dah..

abis makan kita pergi ke secret fashion.. dsuruh pilih baju tp gagenak gw.. gw tolak2 sebisa mungkiinn HHHHHHHHAAAAAAAAAA!!! gagenak abis sumpah --` akhirnya dipaksa pilih.. no.. akhirnya jadi lah 2 pcs tuh baju.. dkasih sama emaknya .. gw langsung cpet2 sms nyokap gue. "mami beliin oleh2 yuk buat si mike n kluarga, gaenak aku dbeliin baju sgala" gyahaha.. dah tu.. abis tu masih ke mol rencana mo nonton avatar 3d tp penuh tmptnya,, kaga jadi d.. akhirnya kita smua balek k guess house tmpat mke nginep.. dsana duduk2 smbil ngobrol2.. jam 7 pergi makan seafood.. makan cumi, kepiting, kerang ampe 2 piring masing2 yg ada dimeja.. kembali gw dicekokin sama kerang, cumi2 suruh abisin n kepiting 1 ekor + 3 capitnya yg gede itu --`

pulank makan jam 8.30 gue lsg dianter k hotel gue nginep.. disana bner2 melentung perut gue..stelah pamitan dll mreka lsg pulank.. krn waktu tu nyampe hotel gue dah malem juga gt..

meskipun kenyang n perut melentung,tp tetep ajah jam 12 gue makan lagi krn dhotel gue ada acara taon baruan hahaha.. sayanknya tgl 1 gue da harus pulank .. pdahal tgl 1 diajakin nonton sm cecenya juga n sm ko alex(pacar ce2nya) sayank dobel date ga ksampean.. --`

kapan yank kita liburan bareng lage hahaha...

yah gw ngerasa srek kok sm kluarganya.. sangad welcome.. smoga nanti kita bs ktemu lagi ya om, tante, cece.. hahaha XD

Minggu, 29 November 2009

Audit judgment journal..

Aha.. tugas literature review yg awalnya membingungkan sudah mulai menemukan titik cerah.. kira2 begini lah kutipan jurnal yg gue dapet di inet, yg udah gue ringkas dan harus gue kumpul sbg tugas kelompok.. T.T

Debiasing Audit Judgment with Accountability

Published in : 1993

Researcher : Jane Kennedy

Research Variable : Audit Judgment, Accountability

Methods

Two subject groups were used. One consisted of 58 executive M.B.A. students at Duke University, all of whom had completed the M.B.A. core course in financial accounting and therefore should be familiar with the accounting concepts used in the experimental materials. Subjects had, on average, 5.5 years of business-related experience. The other group consisted of 171 auditors attending managers' training sessions for a Big Six firm. On average, subjects had been directly involved in six audits in which, as part of an audit team, they judged a client's ability to continue as a going concern. Subjects in both groups were randomly assigned to treatment conditions. Experience did not differ across conditions for either subject group.

The experiment was conducted in a group setting. After subjects read the general instructions, evidence was presented via an overhead projector to ensure that all subjects read the items in the order in- tended, had the same exposure time, and had no opportunity to look back and reread the evidence in some other order. Each slide showed one piece of evidence for nine seconds.9

The task required subjects to judge the likelihood that a firm would fail (i.e., enter bankruptcy proceedings) within one year based on eight pieces of evidence-four supporting failure and four supporting via- bility.10 The items are listed below, where F (V) indicates that the item supports failure (viability).

1. The firm's major product is generally considered to be of good quality. (V)

2. Management states that it is possible that a key patent may be obtained in the near future. (V)

3. This year the company reported a positive cash flow from operations. (V)

4. In general, suppliers of the firm indicate that usual trade credit to the firm will be available. (V)

5. This year the firm reported a significant loss from operations. (F)

6. It appears that if needed it will be difficult to obtain additional debt capital. (F)

7. Discussions with management indicate that a material liability from litigation is likely this year. (F)

8. Management believes there is a good chance of losing a major customer. (F)

To provide a common base rate of failure, subjects were told before considering any firm-specific evidence that the likelihood the firm would fail was 50%. After subjects read the firm-specific evidence, they were asked, "How likely do you think it is that this firm will fail (i.e., enter bankruptcy proceedings) within one year?" Subjects responded on a 0-100 scale, with endpoints labeled "certain this firm will not fail" (0) and "certain this firm will fail" (100) and the midpoint labeled "completely uncertain." The likelihood judgment is the dependent variable. Subjects also completed a brief post experimental questionnaire which included a number of questions designed to check the accountability manipulations.

A 2 x 3 x 2 (order of evidence x accountability x complexity) between subjects experimental design was used. The two orders of evidence were (1) evidence supporting viability followed by evidence supporting failure (++++----), and (2) evidence supporting failure followed by evidence supporting viability (---- + + + +).

The three accountability conditions were no accountability, pre-accountability, and post accountability. In the no-accountability conditions subjects were told:

This study concerns how students with your level of education and experience make judgments. Your judgments will be totally confidential and not traceable to you person- ally. Your responses to the materials will be aggregated and averaged with the responses of others to determine general characteristics of judgment. Please do not identify your- self in any way on these materials. Thank you for your cooperation.

The distinction between pre- and post-accountability is the timing of the accountability manipulation. Pre-accountable subjects were told the following, before evidence for the failure/viability judgment was presented:

This study, sponsored by the Fuqua School, is part of an important effort of the School to enhance the effectiveness and efficiency of business practice. We are interested in learning how students at your level of education and experience make judgments, and in assessing the quality of those judgments. Your responses to the following materials will be reviewed and may be selected for a follow-up conference with you and members of the EEMBA Faculty. If you are selected for this conference, you will be asked to explain and justify your responses. Please print your name and phone number in the space pro- vided so that we can contact you. Thank you for your cooperation.

Post-accountable subjects were presented with the same paragraph after evidence for failure/viability, but before the likelihood judgment was required. Two subject groups were used to operationalize task complexity. Auditors evaluate the ability of a client to continue as a going concern on every audit engagement while executive M.B.A. students, on average, have little experience judging the ability of a firm to survive. Although more complex, this task is not unreasonable for executive M.B.A. students given their business interests and educations.

Analysis and Results

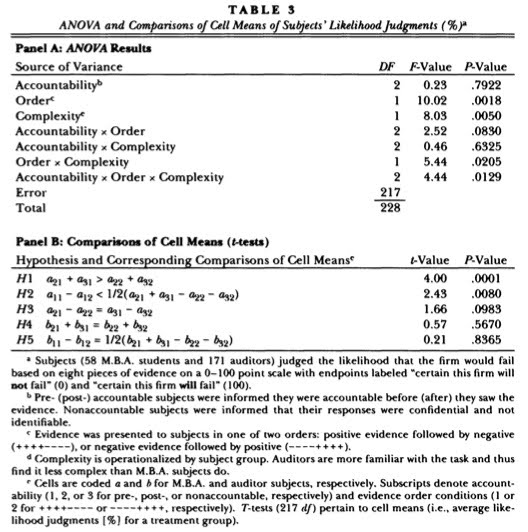

Recall that likelihood judgments were elicited on a 0-100 point scale; thus, subjects' judgments may be thought of as percentages. Descriptive statistics for the likelihood

judgments of M.B.A. and auditor subjects are presented in table 2, panels A and B. The analysis-of-variance (ANOVA) and results of comparisons (protected t-tests) of specific treatment (cell) means are in table 3, panels A and B.18

The ANOVA reveals a significant accountability x order x complexity interaction (F = 4.44, p < .01; table 3, panel A). The test for recency among executive M.B.A. subjects shows that post- and non-accountable subjects who receive evidence in a positive/negative order judge the likelihood of failure to be greater than subjects who receive the same evidence in a negative/positive order (means of 60.6 and 72.5 vs. 46.0 and 37.3, table 2, panel A; t = 4.00, p < .0001, table 3, panel B).

Pre-accountable subjects' likelihood judgments exhibit no recency (mean of 48.5 vs. 50.0, table 2, panel A) in contrast to their post-accountable and non-accountable counterparts (t = 2.43, p < .008, one- tailed, table 3, panel B). Accountability clearly moderates recency among executive M.B.A. students. Hypothesis 3 is weakly supported; recency shown by non-accountable subjects is marginally stronger than that shown by post-accountable subjects (difference between means of 72.5 and 37.2 vs. 60.6 and 46.0, table 2, panel A; t = 1.66, p = .10, table 3, panel B).

An analysis of the frequency of subjects adjusting away from the anchor provides results consistent with those above; 93% of post-accountable subjects and 96% of non-accountable subjects adjusted their likelihood of failure judgments away from the anchor while only 68% of pre-accountable subjects did (X2= 15.24, p < .000).19 Moreover, more (fewer) M.B.A. subjects in the positive/negative condition adjusted their likelihoods up (down) than in the negative/positive condition. The proportions of subjects adjusting up (down) are 72% (14%) and 28% (55%) for the positive/negative and negative/positive order conditions, respectively (x2 = 13.14, p < .001).

In contrast to the results obtained from M.B.A. subjects, auditors' judgments show no recency. The difference between the judgments of post- and non-accountable subjects receiving negative evidence last and those receiving positive evidence last is not significant (means of 45.8 and 44.2 vs. 41.4 and 46.3, table 2, panel B; t = .57, p = .57, table 3, panel B). This result is consistent with EoS processing, i.e., the evidence is considered as a set and the anchor is updated once, for the set, rather than for each piece of evidence in the set. Consistent with H5, auditor judgments were not influenced by pre-accountability requirements (mean of 45.6 vs. 43.5, table 2, panel B; t = .21, p = .84). The frequencies of subjects revising up, down, and not revising from the anchor are approximately equal across all conditions, providing further support for no order or accountability effects among auditors.

Future Research

Future research could examine the interaction of accountability with other pressures on auditors such as those mentioned above. The particular accountability "culture" may also be important. For example, accounting firms may have an atmosphere of accountability that affects all facets of an auditor's work.

Alternatively, accountability requirements may be overtly stressed on each task undertaken. Finally, the framework presented suggests potentially effective means of mitigating data-related biases, which may be the more important of the two types of bias because of their immunity to incentive mechanisms.

Summary

Although recency is not expected for auditor subjects who are familiar with a particular task, recency is a well-documented phenomenon in the audit judgment literature. A review of that research indicates that, for the most part, recency is found when subjects were explicitly required to process the evidence in a step-by-step (SbS) mode or when the task was made more complex so that subjects chose a SbS strategy. These studies did not control for accountability requirements, which are common to many audit judgment settings.

This study had subjects make only one judgment after all evidence was presented (EoS), rather than making a judgment after each piece of evidence was presented (SbS). Recency is hypothesized for judges who use a SbS processing strategy to ease the cognitive demands of complex belief revision tasks in an EoS response mode. Executive M.B.A. subjects, unfamiliar with judging the ability of a firm to survive, exhibited significant recency effects while auditors, who are familiar with this task, did not. However, when accountability was imposed on the M.B.A. subjects, no recency effects were noted. Consistent with the framework proposed in section 2, this experiment shows that effort- related biases such as recency can be mitigated by accountability.

There are at least three limitations of this study. First, auditors work in much richer information environments than depicted in the experiment. It is not obvious, however, what impact additional information has on auditors' judgment biases. Second, accountable subjects faced no penalty for providing unjustifiable responses in this experiment, while in an audit environment unjustifiable judgments could result in additional hours worked, reputation costs, etc. Finally, I examine accountability in isolation from other pressures auditors face (deadlines, incentives, and feedback), all of which may interact with accountability (Ashton [1990] and McDaniel [1990]).

This study has implications for auditing practice and audit judgment research because auditors operate in an accountability-inducing environment. Audit managers make going-concern evaluations of clients based on many pieces of evidence that have been gathered and re- viewed, and their own judgments are subject to review. The absence of recency found here, when judgments were made by experienced professionals after all the evidence was available, and the debiasing effect of accountability for less experienced judges suggest that recency may not be an issue of great concern for audit practitioners. Moreover, ex- periments that do not control for accountability may overstate the significance of judgment biases attributable to effort.

haaa.. akhirnya slese ya :D senanknya... tinggal diringkas jadi table.. n dkumpul k Pak Galumbang... masih nyusul satu lg tugas individu dr pak Butar2... smangad amell hahaha..

Debiasing Audit Judgment with Accountability

Published in : 1993

Researcher : Jane Kennedy

Research Variable : Audit Judgment, Accountability

Methods

Two subject groups were used. One consisted of 58 executive M.B.A. students at Duke University, all of whom had completed the M.B.A. core course in financial accounting and therefore should be familiar with the accounting concepts used in the experimental materials. Subjects had, on average, 5.5 years of business-related experience. The other group consisted of 171 auditors attending managers' training sessions for a Big Six firm. On average, subjects had been directly involved in six audits in which, as part of an audit team, they judged a client's ability to continue as a going concern. Subjects in both groups were randomly assigned to treatment conditions. Experience did not differ across conditions for either subject group.

The experiment was conducted in a group setting. After subjects read the general instructions, evidence was presented via an overhead projector to ensure that all subjects read the items in the order in- tended, had the same exposure time, and had no opportunity to look back and reread the evidence in some other order. Each slide showed one piece of evidence for nine seconds.9

The task required subjects to judge the likelihood that a firm would fail (i.e., enter bankruptcy proceedings) within one year based on eight pieces of evidence-four supporting failure and four supporting via- bility.10 The items are listed below, where F (V) indicates that the item supports failure (viability).

1. The firm's major product is generally considered to be of good quality. (V)

2. Management states that it is possible that a key patent may be obtained in the near future. (V)

3. This year the company reported a positive cash flow from operations. (V)

4. In general, suppliers of the firm indicate that usual trade credit to the firm will be available. (V)

5. This year the firm reported a significant loss from operations. (F)

6. It appears that if needed it will be difficult to obtain additional debt capital. (F)

7. Discussions with management indicate that a material liability from litigation is likely this year. (F)

8. Management believes there is a good chance of losing a major customer. (F)

To provide a common base rate of failure, subjects were told before considering any firm-specific evidence that the likelihood the firm would fail was 50%. After subjects read the firm-specific evidence, they were asked, "How likely do you think it is that this firm will fail (i.e., enter bankruptcy proceedings) within one year?" Subjects responded on a 0-100 scale, with endpoints labeled "certain this firm will not fail" (0) and "certain this firm will fail" (100) and the midpoint labeled "completely uncertain." The likelihood judgment is the dependent variable. Subjects also completed a brief post experimental questionnaire which included a number of questions designed to check the accountability manipulations.

A 2 x 3 x 2 (order of evidence x accountability x complexity) between subjects experimental design was used. The two orders of evidence were (1) evidence supporting viability followed by evidence supporting failure (++++----), and (2) evidence supporting failure followed by evidence supporting viability (---- + + + +).

The three accountability conditions were no accountability, pre-accountability, and post accountability. In the no-accountability conditions subjects were told:

This study concerns how students with your level of education and experience make judgments. Your judgments will be totally confidential and not traceable to you person- ally. Your responses to the materials will be aggregated and averaged with the responses of others to determine general characteristics of judgment. Please do not identify your- self in any way on these materials. Thank you for your cooperation.

The distinction between pre- and post-accountability is the timing of the accountability manipulation. Pre-accountable subjects were told the following, before evidence for the failure/viability judgment was presented:

This study, sponsored by the Fuqua School, is part of an important effort of the School to enhance the effectiveness and efficiency of business practice. We are interested in learning how students at your level of education and experience make judgments, and in assessing the quality of those judgments. Your responses to the following materials will be reviewed and may be selected for a follow-up conference with you and members of the EEMBA Faculty. If you are selected for this conference, you will be asked to explain and justify your responses. Please print your name and phone number in the space pro- vided so that we can contact you. Thank you for your cooperation.

Post-accountable subjects were presented with the same paragraph after evidence for failure/viability, but before the likelihood judgment was required. Two subject groups were used to operationalize task complexity. Auditors evaluate the ability of a client to continue as a going concern on every audit engagement while executive M.B.A. students, on average, have little experience judging the ability of a firm to survive. Although more complex, this task is not unreasonable for executive M.B.A. students given their business interests and educations.

Analysis and Results

Recall that likelihood judgments were elicited on a 0-100 point scale; thus, subjects' judgments may be thought of as percentages. Descriptive statistics for the likelihood

judgments of M.B.A. and auditor subjects are presented in table 2, panels A and B. The analysis-of-variance (ANOVA) and results of comparisons (protected t-tests) of specific treatment (cell) means are in table 3, panels A and B.18

The ANOVA reveals a significant accountability x order x complexity interaction (F = 4.44, p < .01; table 3, panel A). The test for recency among executive M.B.A. subjects shows that post- and non-accountable subjects who receive evidence in a positive/negative order judge the likelihood of failure to be greater than subjects who receive the same evidence in a negative/positive order (means of 60.6 and 72.5 vs. 46.0 and 37.3, table 2, panel A; t = 4.00, p < .0001, table 3, panel B).

Pre-accountable subjects' likelihood judgments exhibit no recency (mean of 48.5 vs. 50.0, table 2, panel A) in contrast to their post-accountable and non-accountable counterparts (t = 2.43, p < .008, one- tailed, table 3, panel B). Accountability clearly moderates recency among executive M.B.A. students. Hypothesis 3 is weakly supported; recency shown by non-accountable subjects is marginally stronger than that shown by post-accountable subjects (difference between means of 72.5 and 37.2 vs. 60.6 and 46.0, table 2, panel A; t = 1.66, p = .10, table 3, panel B).

An analysis of the frequency of subjects adjusting away from the anchor provides results consistent with those above; 93% of post-accountable subjects and 96% of non-accountable subjects adjusted their likelihood of failure judgments away from the anchor while only 68% of pre-accountable subjects did (X2= 15.24, p < .000).19 Moreover, more (fewer) M.B.A. subjects in the positive/negative condition adjusted their likelihoods up (down) than in the negative/positive condition. The proportions of subjects adjusting up (down) are 72% (14%) and 28% (55%) for the positive/negative and negative/positive order conditions, respectively (x2 = 13.14, p < .001).

In contrast to the results obtained from M.B.A. subjects, auditors' judgments show no recency. The difference between the judgments of post- and non-accountable subjects receiving negative evidence last and those receiving positive evidence last is not significant (means of 45.8 and 44.2 vs. 41.4 and 46.3, table 2, panel B; t = .57, p = .57, table 3, panel B). This result is consistent with EoS processing, i.e., the evidence is considered as a set and the anchor is updated once, for the set, rather than for each piece of evidence in the set. Consistent with H5, auditor judgments were not influenced by pre-accountability requirements (mean of 45.6 vs. 43.5, table 2, panel B; t = .21, p = .84). The frequencies of subjects revising up, down, and not revising from the anchor are approximately equal across all conditions, providing further support for no order or accountability effects among auditors.

Future Research

Future research could examine the interaction of accountability with other pressures on auditors such as those mentioned above. The particular accountability "culture" may also be important. For example, accounting firms may have an atmosphere of accountability that affects all facets of an auditor's work.

Alternatively, accountability requirements may be overtly stressed on each task undertaken. Finally, the framework presented suggests potentially effective means of mitigating data-related biases, which may be the more important of the two types of bias because of their immunity to incentive mechanisms.

Summary

Although recency is not expected for auditor subjects who are familiar with a particular task, recency is a well-documented phenomenon in the audit judgment literature. A review of that research indicates that, for the most part, recency is found when subjects were explicitly required to process the evidence in a step-by-step (SbS) mode or when the task was made more complex so that subjects chose a SbS strategy. These studies did not control for accountability requirements, which are common to many audit judgment settings.

This study had subjects make only one judgment after all evidence was presented (EoS), rather than making a judgment after each piece of evidence was presented (SbS). Recency is hypothesized for judges who use a SbS processing strategy to ease the cognitive demands of complex belief revision tasks in an EoS response mode. Executive M.B.A. subjects, unfamiliar with judging the ability of a firm to survive, exhibited significant recency effects while auditors, who are familiar with this task, did not. However, when accountability was imposed on the M.B.A. subjects, no recency effects were noted. Consistent with the framework proposed in section 2, this experiment shows that effort- related biases such as recency can be mitigated by accountability.

There are at least three limitations of this study. First, auditors work in much richer information environments than depicted in the experiment. It is not obvious, however, what impact additional information has on auditors' judgment biases. Second, accountable subjects faced no penalty for providing unjustifiable responses in this experiment, while in an audit environment unjustifiable judgments could result in additional hours worked, reputation costs, etc. Finally, I examine accountability in isolation from other pressures auditors face (deadlines, incentives, and feedback), all of which may interact with accountability (Ashton [1990] and McDaniel [1990]).

This study has implications for auditing practice and audit judgment research because auditors operate in an accountability-inducing environment. Audit managers make going-concern evaluations of clients based on many pieces of evidence that have been gathered and re- viewed, and their own judgments are subject to review. The absence of recency found here, when judgments were made by experienced professionals after all the evidence was available, and the debiasing effect of accountability for less experienced judges suggest that recency may not be an issue of great concern for audit practitioners. Moreover, ex- periments that do not control for accountability may overstate the significance of judgment biases attributable to effort.

haaa.. akhirnya slese ya :D senanknya... tinggal diringkas jadi table.. n dkumpul k Pak Galumbang... masih nyusul satu lg tugas individu dr pak Butar2... smangad amell hahaha..

Langganan:

Postingan (Atom)